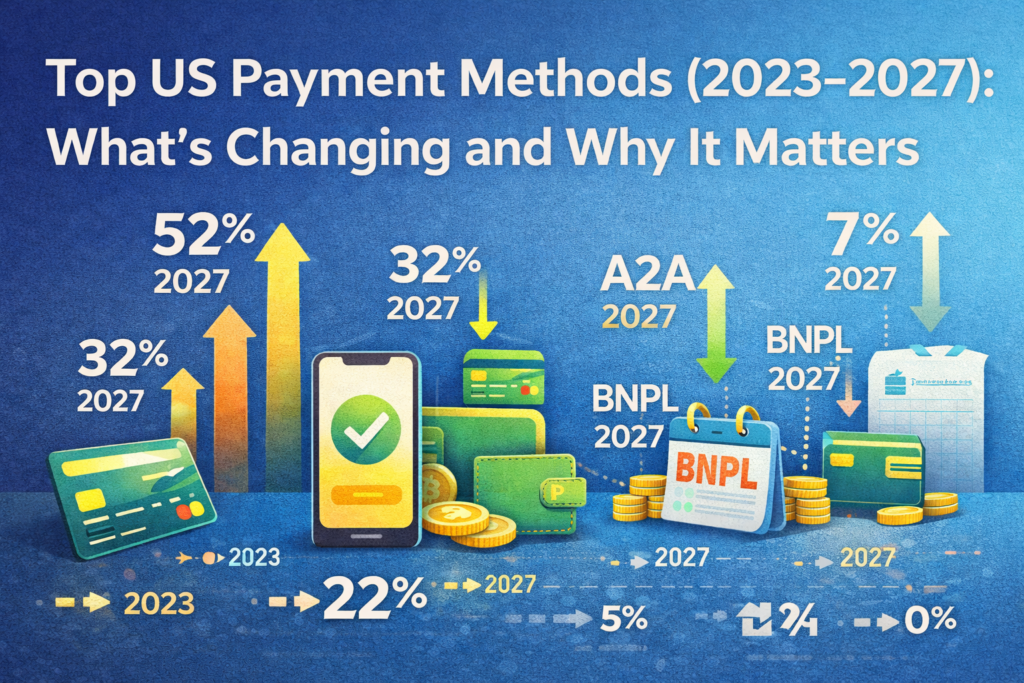

The way Americans pay, both online and in-store, is changing faster than ever. With a swipe, tap, or face scan, consumers are saying goodbye to traditional methods like cash and embracing smarter, faster alternatives. If you're running a business or just curious about where payments are heading, now's the time to understand how e-commerce payment …